Last week I discussed interesting research papers presented at the PCAOB’s Center for Economic Analysis third annual Economic Conference on Auditing and Capital Markets. In order to make this topic a little more enjoyable, I have divided up the presented papers into two posts. Today’s post, part two, will focus on the remaining three research papers presented at the conference.

Research presented

Following is the abstract from each research paper:

1. Assessing Initiatives to Improve the Quality of Group Audits Involving Other Auditors

One of the major current concerns of regulators internationally is the quality of the auditing of multinational groups, particularly those involving the coordination by the principal auditor of other auditors. These concerns resulted in changes to the international auditing standard on group audits, International Standards on Auditing (ISA) No. 600, which are consistent with current initiatives being considered by the PCAOB. The researchers examined audit quality pre and post-ISA 600 to help inform the International Auditing and Assurance Standards Board (IAASB) as to the efficacy of the ISA 600 amendments and inform the PCAOB with regard their similar initiatives under consideration. The researchers made use of unique Australian disclosures which allowed them to identify the nature and extent of involvement of other auditors in group audits. They found that the revisions to ISA 600 have contributed to an improvement in audit quality, specifically for clients of non-Big N (e.g., Big 4) auditors. Further, they found that the quality of multi-national enterprise (MNE) group audits involving other auditors from the same network is lower, and this appears not to be affected by the ISA 600 revisions. Consistent with regulatory concerns, the researchers also examined whether there are any incremental costs for group audits involving other auditors. While the researchers found that group audits involving other auditors are more costly, they did not find evidence of an increase in audit fees associated with these regulatory initiatives.

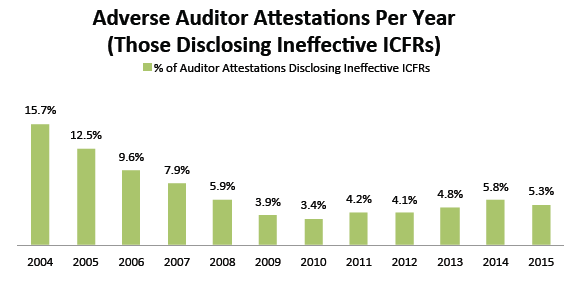

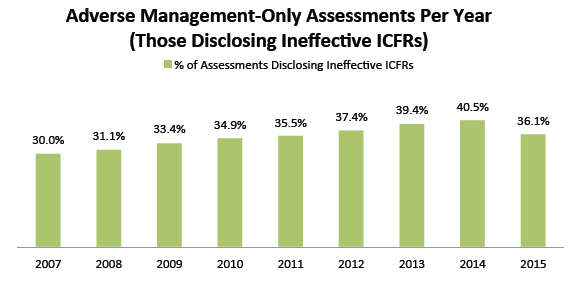

The authors investigated the benefits and costs of exempting firms from auditor oversight of internal control effectiveness disclosures (Section 404(b) of the Sarbanes-Oxley Act of 2002), which I touched on in a previous post. They measured the benefit of exemption with audit fee savings, which the authors estimated to be an aggregate $388 million from 2007 to 2014 for their sample of exempt firms. The key concern of exemption is internal control misreporting (i.e., firms with ineffective internal controls disclose effective internal controls). Misreporting imposes at least two measurable costs on current and prospective shareholders: lower operating performance due to non-remediation, and market values that fail to reflect a firm’s underlying internal control status. The authors calculated the cost of 404(b) exemption from 2007 to 2014 to be an aggregate $856 million in lower future earnings due to non-remediation, and a $935 million delay in aggregate market value decline due to untimely internal control disclosure. Although the aggregate costs of exemption exceed the benefits, the costs are borne by shareholders of only a fraction of exempt firms, whereas the audit fee savings are shared by all.

In addition to yielding evidence on the benefits and costs of internal control disclosure regulation, their study provides a prediction model for identifying the firms most at risk of inaccurately disclosing internal controls. The prediction model predicts that approximately 20.2% of exempt firms should disclose ineffective internal controls, whereas only 10.9% do so. Thus, the authors infer that 46% of exempt firms that maintain ineffective internal controls fail to discover or disclose it.

3. Tell Me More: A Content Analysis of Expanded Auditor Reporting in the United Kingdom

This study examined the effect of expanded audit disclosures required by ISA 700 (UK and Ireland), The Independent Auditor’s Report on Financial Statements, on the communication value of the audit report. Using content analysis measures, readability and tone, as proxies for communication value, the author found that in the post-ISA 700 period: 1) audit report readability improves and 2) audit report tone changes with a higher occurrence of negative and uncertain words. The author also evaluated analyst behavior in response to the ISA 700 audit report and found that analyst forecast dispersion decreased in the post-ISA 700 period. In additional analyses, the author showed that Big N and industry expert auditors wrote audit reports that are more readable. The author also found that domain-specific word dictionaries, generated from SEC Form-10K’s and earnings press releases, have a lower frequency in audit reports in both the pre and post-ISA 700 period.

With the heightened global interest in improving the historical pass/fail audit report, these results show that expanded audit disclosures can be communicated in a manner that is accessible and meaningful to the financial statement user.

In summary

Again, we find similar take-aways from these academic papers, which shed light on the impact that professional standards have on audit firms and their clients.